When bankers talk about “small business customers,” the mental picture is often the same:

A bustling local business with a loyal customer base, a team of employees, a healthy revenue stream, and a finance team running an accounting or ERP system like clockwork.

In short

- Only about 9% of small businesses earn more than $1M annually — the vast majority operate with thin margins, no back office, and real-time financial decisions.

- Most business checking products were designed for mid-sized and larger commercial clients, not the HVAC business or wedding photographer who actually makes up the market.

- Every time a small business turns to an outside provider for payments, accounting, or lending, another third party builds the relationship that could belong to the bank.

- A modern checking account that handles receivables, payables, reporting, and access to capital becomes the single trusted hub — and the natural cross-sell path for traditional lending.

The truth? That describes only a small fraction of the small business market.

What do the numbers actually say about the small business market?

According to the SBA and FDIC, only about 9% of small businesses earn more than $1 million annually. That means over 90% are making less — often much less. In fact, non-employer firms, which make up 82% of all small businesses, report an average annual revenue of under $50,000.

Even among employer firms, the majority have between one and four employees. These are local trades, consultants, food truck operators, and professional service providers. They are deeply rooted in their communities but often operating with thin margins, wearing multiple hats, and making financial decisions in real time.

This isn’t just a demographic footnote — it’s the reality for millions of businesses. And it means that the “small business” accounts sitting in your portfolio are more likely to represent micro-firms or solo entrepreneurs than companies in the $2–5 million revenue range.

Where is the experience gap in small business banking today?

Here’s where the challenge emerges:

Most business checking products were designed with mid-sized and larger small businesses in mind — the ones already moving significant cash, using treasury services, and applying for larger loans.

For the rest of the market — the HVAC business with two employees, the wedding photographer working from home, the landscaper with a pickup truck and a helper — the checking account experience often feels like an afterthought. They might have:

- A free business checking account with few value-added features such as bill pay and mRDC.

- Or worse, a personal checking account they use for business because they can’t see the benefit of switching.

Meanwhile, many of these business owners are forced to cobble together their essential workflows that also include accepting customer payments, accounting, financial record keeping, and financing growth. Often, this means turning to non‑bank providers to fill the gaps, relying on:

- Square or PayPal for card acceptance.

- Spreadsheets for tracking expenses.

- A separate lender — often not their bank — for working capital.

Every one of those tools is an opportunity for a third party to build a relationship and capture revenue that could belong to the bank.

Why is lending such a challenge for under-$1M businesses?

Lending is another area where micro and small businesses face persistent challenges. Even when they have a strong relationship with a bank, the process of applying for and receiving credit is often slow, disconnected, and geared toward larger firms.

Many of these smallest businesses — especially those under $1 million in annual revenue — end up financing their growth in less-than-ideal ways. Surveys from the Federal Reserve and other industry sources show that a significant share rely on personal credit cards, personal savings, or loans from friends and family. Others turn to alternative online lenders, merchant cash advance providers, or fintech platforms that promise speed and simplicity, even if the cost is higher. These choices are often driven by the difficulty of qualifying for traditional bank credit, the length of the approval process, and a lack of tailored lending products.

The FDIC’s small business lending data confirms that smaller-revenue firms are less likely to be approved for bank loans, even though they have pressing needs:

- Covering cash flow gaps between receivables and payables.

- Investing in new equipment.

- Hiring their first employee.

- Launching a marketing campaign.

For these businesses, even a small loan or line of credit can make the difference between plateauing and growing. Yet too often, they turn to sources outside their primary bank — especially online lenders and fintechs — that can meet them where they are, quickly and digitally.

What does the opportunity look like when the dots connect?

When you step back and connect the dots, the picture becomes clear:

The majority of small businesses in your market are under $1 million in annual revenue. Most have small teams or no employees at all. Many do not use accounting software, rely on manual processes, and lack easy access to credit.

And yet — these are the very businesses that represent your largest growth opportunity.

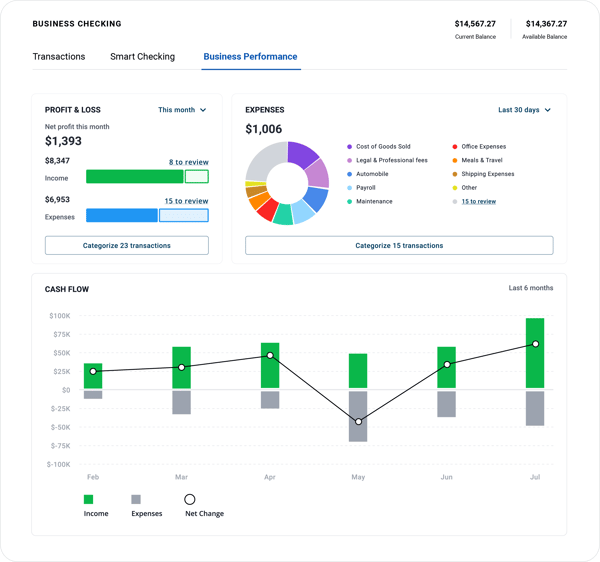

Imagine offering a business checking account that does more than hold deposits:

- It lets a business send professional invoices and get paid online.

- It offers built-in payment acceptance for card, ACH, and in-person sales.

- It Integrates accounting functionality into the account experience.

- It tracks cash flow and produces real-time financial reports.

- It provides fast access to working capital — without sending the customer to a third party and supporting a starting place for traditional bank lending.

For the business owner, their business checking account becomes the single, trusted hub for managing their money, customers, and growth. For the bank, it’s a deeper relationship, more engaged accounts, and a natural pathway to cross-sell lending and other services.

Why does this have to happen now?

Fintechs aren’t waiting to serve this segment. Bluevine has expanded from online lender into banking and payments. Square is courting brick-and-mortar merchants with banking services. Stripe is embedding financial products into digital storefronts.

If banks don’t step in with a modern, integrated business checking experience, these third parties will continue to capture the daily financial relationship — and the lifetime value — of your small business customers.

Bottom line:

The under-$1M revenue business market is massive, underserved, and ready for a better solution. By designing a business checking account with the tools they need to operate — all in one place — your bank can seize this opportunity before someone else does.

Frequently asked questions

How big is the under-$1M small business segment?

Roughly 91% of U.S. businesses earn under $1M in annual revenue, and the 82% that are non-employer firms report average annual revenue under $50,000. It's not a niche — it's the mainstream of small business.

Why does the traditional checking account fall short for these businesses?

Business checking was built for companies with finance staff, treasury needs, and larger loans. Under-$1M businesses need to send invoices, accept payments, track cash flow, and access small amounts of capital fast — and most banks don't offer that natively.

What do under-$1M businesses do today to fill the gap?

They piece workflows together across Square or PayPal for card acceptance, spreadsheets for expenses, and alternative lenders for working capital — each of which is an opportunity for a non-bank to build the primary operating relationship.

What does a modernized business checking account produce for the bank?

Deeper engagement, stickier relationships, natural cross-sell into lending and treasury, and meaningful non-interest income — all from a segment that already exists inside the portfolio.

Why is now the moment?

Square is expanding into banking, Bluevine has moved from lending into deposits, and embedded finance is making it faster than ever to stand up a modern offering. The segment will not stay underserved much longer — the question is who serves it.